A look at the IEA’s “Oil Medium-Term Market Report 2015”

On Tuesday 10 February at 13:00 GMT the IEA released its “Oil Medium-Term Market Report 2015″. The day before the release I was contacted by Jens Ergon at Sveriges Television (“Sweden’s Television, SVT) who wanted to get my opinion on the report. I had some hours to read through the 140 pages of the version provided to media before the report’s official release. It meant that I could comment on the report immediately it was released. SVT has now reported some of those comments in an article that Jens Ergon has written, “The Price Crash Will Reshape The Oil Market.” The subtitle is, “American oil boom behind the falling price. But opinions vary widely on the future of oil.”

Let’s now go through the article together, and I will make a few comments as we do so.

“The significant fall in the price of oil has taken the world’s experts by surprise. Since the summer of 2014, the price of oil has more than halved from over $100 per barrel to a price today of around $50. Last Tuesday the International Energy Agency, IEA, made its first report since the price fall. In the report, the development is described as the beginning of a new era. The IEA’s press release that accompanied the release of the report stated, “The recent crash in oil prices will cause the oil market to rebalance in ways that challenge traditional thinking about the responsiveness of supply and demand.”

– What is surprising is not that the oil price has fallen but the severity of the drop and that it has continued during half a year until up to a few weeks ago”, commented Daniel Spiro, an economist with a focus on price developments for oil and natural resources at Oslo University.”

If we look back in time, there were similar price falls at the beginning of the 1980s and in 2008. For economists, the price fall was as surprising then as it is now. The interesting thing is that there has always been a good explanation for their occurrence, but economists are poor at predicting when a fall will occur. I have chosen never to predict the price of oil but to say always and only that, “the price will be what the market is prepared to pay.”

“From end of cheap oil to price crash

The price crash comes after some years of historically high prices. Except for the transient fall that occurred with the financial crisis of 2008-9 the oil price rose steeply during the entire first decade of this century and stayed at around $100 until the summer of 2014. It contrasts with the price of around $20 per barrel during the 1990s. Some researchers have regarded the high oil prices as a sign of Peak Oil, i.e. that the rate of global oil production is near the maximum that is geologically possible. Others have doubted the concept of Peak Oil and asserted that the higher prices would only encourage new, if more expensive, oil production. Data such as that published by the IEA clearly show that the easily produced, so-called “conventional oil” reached maximum production several years ago – at around 70 million barrels per day. But during recent years the introduction of more expensive, so-called “unconventional oil” – such as from the Canadian tar sands and, foremost, US shale oil – has compensated for the fall in conventional oil and has allowed total world oil production to increase somewhat, to just over 74 million barrels per day.”

During the 1990s the oil price even fell below $10 per barrel. It was in 1998 that Colin J. Campbell and Jean H. Laherrère published their famous article, “THE END OF CHEAP OIL” in the journal Scientific American at the same time as The Economist wrote that the world was “Drowning in oil.” See my blog “How cheap is oil today?”. Colin and Jean wrote that cheap oil would reach a production maximum in around 2004 and today we know that the conventional oil that was cheap in 1998 peaked in 2005. From 1998 until 2008 the price of oil rose from $10 per barrel to $147 per barrel. The era of cheap oil was over. Typically, economists interpret such a price increase as a sign of scarcity, and in this case, we can call this shortage “Peak Oil.” Despite that, many use any argument, no matter how contrived, to assert that Peak Oil lies far in the future.

Today, many people regard $50 per barrel oil as cheap and as a sign that we are, once again, “drowning in oil.” According to BP, production of crude oil and natural gas liquids totaled 82.6 Mb/d in 2006. If that production had continued at the same rate during the following ten years, then the additional of oil would have raised total production to 92.3 Mb/d in 2013. Instead, 2013 saw the total production at 86.8 Mb/d. The increase of 4.2 Mb/d we saw from 2008 to 2013 was not cheap oil. It came from deepwater, from Canada’s oilsands and as NGL and shale oil from fracking in the USA. We can see now that Colin and Jean’s 1998 predictions have proven entirely correct.

As you can see in the figure, conventional crude oil reached maximum production in 2005-6 at 70 Mb/d and today is down at 67-8 Mb/d if one includes deepwater oil production as conventional. But deepwater production is expensive. If one also includes oil from oil sands and shale oil, then the total production rate reaches 74 Mb/d. Note that NGL is not included in these numbers.

“US shale oil is decisive

A common perception in the oil industry has thus been that the era of ‘cheap’ oil is over. The question is if that perception has been overturned by the dramatic price fall. Kjell Aleklett, a professor in Uppsala and one of the leading researchers behind the theory of Peak Oil, is one of those who does not believe so.

– One must remember that the idea of what is ‘cheap’ oil differs markedly today from what it was 15-20 years ago. During the 1990s a price of around $10-15 was ‘cheap oil.’ Today $50 is regarded as cheap, but it would have been regarded as sky high back then, comments Aleklett.

According to the IEA’s recent report, the expansion of shale oil production is a decisive factor behind the fall in price. Together with reduced expectations of world growth and oil consumption, the shale oil boom in the USA has led to an imbalance and a temporary overcapacity in oil production. According to the IEA, another significant factor is that OPEC including Saudi Arabia (contrary to the expectations of many) have not attempted to oppose the price fall by reducing their production.”

Between 2005 and the present day the USA’s consumption of oil has declined by 2 Mb/d. Two reasons for this are the blending of ethanol into gasoline and that today’s new cars in the USA use approximately 25% less fuel per kilometer than they did ten years ago. By 2014 shale oil production had grown to about 4 Mb/d and if we include condensing the figure is 5.6 Mb/d. Compared with 2005 the USA has reduced its need for oil imports by 7 Mb/d which is a volume similar to the entire export volume of Saudi Arabia. The reduction is by 5.5% per year. A reduction with 7 Mb/d amounts to a reduction of 2.6 billion barrels. During the same period, the oil price has been around $100 per barrel which means that the USA’s trade balance since 2005 has improved by $260 billion per year. It is mainly this reduced need for imports that has led to the current oversupply of oil on the world market.

“Historical change in OPEC

One way of describing these developments is that OPEC has, for the moment, given up its role as a price cartel and so-called ‘swing producer.’ Instead, they have continued to produce oil at their maximum rate and have allowed the market to set the price.

– If the OPEC nations continue to produce flat out then, this is a historic change. In that case, the organization will lose, for all practical purposes, its significance, says Aleklett.

There has been considerable speculation regarding OPEC’s recent inaction. However, it is clear that the price fall has hindered costly investments and damaged high-cost producers – and those oil exporting nations that have become dependent on a high oil price. Russia is such a nation. According to the IEA, Russia now stands before a ‘perfect storm’ with falling oil production as a consequence. Canada’s oil sands are another example. And – to an uncertain extent – the USA’s production of shale oil.

– One can speculate regarding why OPEC has done this. But an interesting hypothesis is that Saudi Arabia is concerned regarding ‘demand destruction,’ i.e. competition from an increasing number of alternatives to their easily produced, cheap oil and in particular from shale oil. But Saudi Arabia’s actions could also be addressing a longer-term threat from renewable alternatives. Or a combination of these reasons. By allowing the price to fall, Saudi Arabia is hoping to undermine their competitors, says Daniel Spiro.”

In the 1930s there was an overproduction of oil in Texas, and the price sank dramatically. It was then decided that the Railroad Commission of Texas (RRC) would limit oil transport to a suitable volume to increase the price. They did this until the end of the 1960s when the demand for oil finally exceeded production capacity. It was then time to abandon that system. However, it was the RRC’s system that inspired some oil producing nations to form the OPEC cartel. When the OPEC countries reach their maximum rate of oil production or no longer care about regulating oil production, then OPEC’s main reason to exist disappears.

There is no doubt that the fracking industry has reacted very quickly. The basis for the industry is that thousands of new wells must be drilled every year. The company Baker Hughes releases weekly reports on how many drilling rigs are operating and what they are drilling for. In 2008 the price of oil fell as dramatically as it has done recently. Back then, over half of the operating drilling rigs were idled within six months. Now, in the last three months, we see that 25 % of the rigs have been idled. By summer, certainly half of the rigs that were drilling in October 2014 will be idled, and half of the jobs in that part of the industry will have disappeared. In 2008-9 it was mainly rigged drilling for gas that was idled, but there was also a reduction in rigs drilling for oil. If no new wells are drilled, then the decrease in production from the fracking fields will be about 40% per year. A few new wells will be opened in coming months but then fewer and fewer. If the oil price stays at the current low level, then the USA’s oil production at the beginning of next year will be around 1 Mb/d lower than it is today. The frackers will become the ‘swing producers’”.

“Increasing threat of stranded assets

“There is a rapidly growing discussion within the oil industry regarding what are called ‘stranded assets’ – the fact that the larger part of the world’s fossil fuel reserves cannot be produced if the world is to avoid severe climate change. New calculations presented in the journal Nature in January show that 80% of the world’s coal reserves and one-third of the world’s oil reserves cannot be used, at least not before 2050.

With renewable energy advancing and a new global climate treaty in sight in 2015, the question is being asked, who will be left holding the bag when this type of stranded asset becomes a reality. According to the article in Nature, the cheapest option for the world would be, in principle, if all unconventional oil was left on the ground. But also 40% of the oil in the Middle East. Tomas Kåberger, the former head of the Swedish Energy Agency and currently professor of energy and the environment at the Chalmers University of Technology, is one of those who sees the oil price fall and OPEC’s actions as a sign of instability in the fossil fuel industry.

– I believe we see the consequences of technical developments that will rapidly make energy cheaper and primarily renewable energy. It is a change on a broad front: cheaper electricity from the sun and the wind, cheaper electric cars and more efficient fossil fuelled cars. This is a change that few believed was possible only a few years ago. And it significantly reduces the prospects for future oil consumption. For the fossil fuel industry this means a dramatic change, said Kåberger.”

That the Middle East’s oil should remain underground because we do not need it in future is still wishful thinking. We see that renewable energy is making inroads and replacing fossil fuels, but some of the success of renewable energy sources is due to tax exemptions. Currently, taxation income from the fossil fuel industry is an important part of the budget for European nations.

Renewable energy is making inroads into electricity production, but there also exists a tradition of renewable energy production by the expansion of hydroelectric power. Marginal production of renewable energy is important, not least to put downward pressure on other forms of energy. In that way, subsidization of renewable energy is a good investment.

“Price prognoses vary widely

So what will happen during the coming year? Will the threat of Peak Oil and rising oil prices be disarmed by technological developments where increasingly cheap alternatives to oil instead begin to challenge the oil industry? Will low oil prices continue – or will prices recover – and, if so, how fast and to what level?

Within the oil industry, predictions vary widely. According to Bloomberg the price range for oil in 2015 will lie between $35 and $80 – and during coming years the spread of predictions covers everything between $20 and $200. The uncertainty is greater than seen for a long time.

– If you asked me I would not like to venture a much more precise price range than that. The price of oil has shown itself to be very sensitive, asserts Daniel Spiro.

In its report, the IEA is counting on a moderate recovery of oil prices during the next five years, to $70-80 per barrel.

– This response to the low oil prices is an example of how shale oil has changed the entire oil market. OPEC’s behavior in letting the market balance itself is another example. This can make shale oil the new ‘swing producer’ but will not force it out of the market, says the IEA’s head Maria van der Hoeven.”

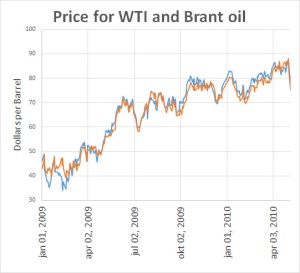

When it comes to the price of oil, I usually do not express an opinion and the fluctuations we have seen in recent years recently show this to be a sensible decision. In the graph, you can see how the oil price recovered in 2009.

“Maximum production or dwindling oil consumption?

Kjell Aleklett is skeptical of the IEA’s future progress. According to Aleklett neither shale oil nor the price crash of the past six months negates the fact that the world finds itself near Peak Oil.

– The IEA assumes that oil production in the world will continue to grow by just over 1% per year. At the same time, production from today’s conventional oil fields is falling steadily. I cannot see how this equation works.

– According to Aleklett, there is an excessive belief in shale oil’s possibilities. Its production requires the continuous drilling of new wells – something that the price fall is now putting an end to.

– The price fall involves two things. One consequence is to freeze investment in the discovery of new oil the world over. The other is that it wallops US shale oil production. I believe we will see a top in shale oil production already this year. Ironically, the fall in the oil price may bring forward Peak Oil. I would not be surprised if maximal world oil production ultimately occurs this year or next year, said Aleklett.

– I agree with Aleklett that there is extreme confidence around shale oil. And I think that he has some valid points with his analysis of Peak Oil. But I believe that the market shift we are now witnessing is fundamentally due to that alternative to oil are becoming increasingly cheaper. And that is a revolutionary development that in principle is impossible to stop, asserts Kåberger.”

To conclude Jens Ergon discusses ‘Peak Oil.’ All agree that we passed the maximum of conventional oil production in 2005-6 (see graph above). What remains to discuss is so-called ‘natural gas liquids’ (NGL), oil sands and shale oil. The greater part of NGL is used in the chemical industry, but the heaviest components of it are blended with oil from the oil sands so make a less viscous liquid that can be transported in pipelines. A large part of NGL-production is a byproduct of shale gas and shale oil production. A reduction in shale oil may bring a reduction in NGL production. Production of oil from oil sands has been hit hard by the low oil prices, but those projects that are underway will probably continue while there will be a dearth of new projects. If the oil price does not recover quickly, then production of shale oil will decline in the coming year.

The IEA says in its ‘Midterm report’ that demand that was 92.43 Mb/d in 2014 will increase to 99.05 Mb/d by 2020. It is an increase of 6.6 Mb/d. In the World Energy Outlook report, they show a collective production decline for all the fields currently producing conventional oil at 6% per year which is the same number that Global Energy Systems in Uppsala reported in 2008. If one considers that currently producing fields will be subject to investment to maintain production, then this decline may be limited to 4 Mb/d per year. It means that the current conventional production of 68 Mb/d will decline by 15 Mb/d by 2020. So we can see that more than 20 Mb/d of the new production is needed for the demand that the IEA envisages. During this short period, there are no new fields that can contribute to this since six years is too short a time frame for bringing new fields online offshore, where such new fields typically lie.

One field that will contribute new oil by 2020 is Johan Sverdrup in Norway. When it is brought online in 2019, it is expected to provide 0.32 to 0.38 Mb/d. To bring online new production equivalent to 20 Mb/d requires very large investment and the cheap oil that contributes to oil companies’ investment budgets will be decreasing. If they prioritize development of discovered fields, there will be less money available to invest in finding new fields. During the period 2020-2030, it will be extremely expensive and difficult to bring new oil production online. There is an economic limit beyond which oil is left underground. The advantage with conventional oilfields is that one has steady (plateau) production for many years and a temporary fluctuation in price thus has less effect on the project. One can even include price volatility in the project plan.

The year that we reach Peak Oil, we will produce more oil than we have ever done previously. We may well feel that the market is oversupplied with oil in that year, just as we do now. The Peak Oil that we now discuss is the peak of unconventional oil production. Since production of this type of oil is very price sensitive the oil market will be a factor contributing to when we reach the global peak of all oil production. There are strong indications that 2015/2016 may see this global peak. In any case, we are certainly on a production plateau compared with the increase in oil production that we saw from the 1980s until 2006.

(Discussions on Aleklett’s Energy Mix)